Customer Due Diligence: Explanation and Benefits

Fraud is a major risk factor across different industries today, with around $485.6 billion lost globally to fraud-related crimes in 2023. This is why various measures to mitigate fraud and other financial crimes have been established. One of these is Customer Due Diligence (CDD), a key component of Know Your Customer (KYC) initiatives.

This article discusses the meaning of Customer Due Diligence, and explores its types, key requirements, processes, and why it plays a vital role in fraud management.

What is Customer Due Diligence (CDD)?

Customer Due Diligence or CDD is the practice of identifying and verifying a customer’s identity to ensure that they are legitimate and accurately assess the risk they pose.

CDD is closely related to what KYC is in that they both aim to learn about a client. However, a big difference between the two is that KYC only occurs at the start of the relationship.

The CDD process also starts at the beginning of a business relationship, but it continues throughout the length of the relationship. Financial institutions continuously monitor their customers’ behavior and update their risk profile accordingly. This practice is key to detecting and addressing suspicious or fraudulent activities immediately.

There are three primary types of CDD that customers may revolve in depending on their activities and risk profiles:

-

Simplified Due Diligence (SDD)

SDD is the most basic level of verification, requiring only basic information and KYC documents from clients, such as proof of identity (e.g., passport or government-issued ID), proof of address (e.g., utility bills), and proof of income (e.g., pay slips or Certificate of Employment). This is applied to clients that carry relatively low risk of money laundering or fraud.

-

Standard Due Diligence

The Standard Due Diligence is applied to most customers with an average risk. It involves standard identification and verification processes, usually done to verify the client’s identity and understand their business nature or source of funds, as well as the risks associated with it.

-

Enhanced Due Diligence (EDD)

EDD is applied to high-risk customers, where there is a higher potential for fraudulent activities or money laundering. EDD requires more comprehensive information, in-depth investigation of the client’s identity and business, as well as more frequent transaction monitoring.

What is the Customer Due Diligence Process?

The CDD process involves several steps designed to ensure comprehensive risk assessment and to respond to the client’s risk level. The process should include these steps:

-

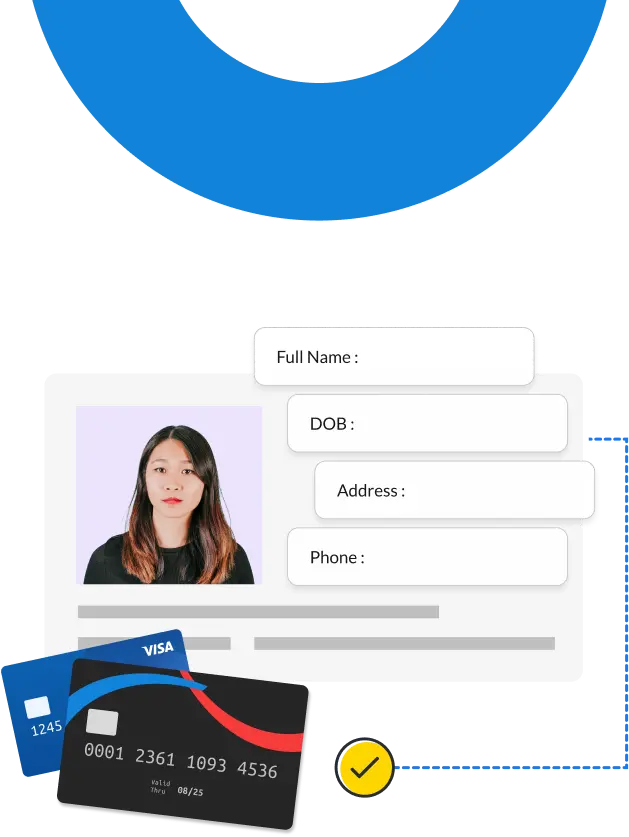

Establishing Customer Identities

This initial step involves collecting the necessary identification documents from the customer and verifying their authenticity. This step can be streamlined through digital processes. eKYC allows clients to upload their data online and automate the verification process, thus allowing for faster onboarding for clients.

-

Performing a Customer Risk Assessment

Once the customer's identity is verified, the next step is assessing their risk for fraud or other financial crimes. For example, GoPay Data evaluates various factors such as the customer's geographical location, type of business, transaction patterns, and any media reports to uncover any red flags. Customers are then categorized into risk levels (low, medium, high) based on the findings of the risk assessment.

APIs for lending assess another type of risk – they determine the customer’s financial capacity to minimize the risk of defaults on top of evaluating risk for fraud. -

Collecting Additional Information (if required)

For high-risk customers, additional information may be needed, triggering Enhanced Due Diligence processes. This could include detailed financial statements, sources of funds, or business plans. These additional documents go through the verification and risk assessment processes again.

-

Continuous Monitoring

If the institution proceeds with starting a business relationship with the client, the CDD process requires continued vigilance for any suspicious activity. Institutions are required to keep track of clients’ transactions and behavior, which can be accomplished through APIs for digital banking and merchant link.

-

Reporting Suspicious Activity

Anti-Money Laundering Regulations (though they differ per country or region) require financial institutions to report any suspicious activities to the relevant authorities. Suspicious activities include unusual transaction patterns, large cash deposits, or any activities that do not match the customer’s known profile.

What is the Importance of CDD in Fraud Management?

As a key component of KYC, Customer Due Diligence is vital to preventing fraud across various industries including banking and finance, real estate, legal, and healthcare. CDD provides a robust framework for detecting and preventing fraudulent activities.

· CDD has a proactive approach to risk management, thus allowing for early detection of any fraudulent activity.

· CDD enables financial institutions to assess the risk associated with each customer accurately, which is key to effective risk mitigation.

· CDD processes enhance the overall security of finance and banking institutions, protecting both institutions and customers.

· CDD is not only a requirement but its processes help ensure compliance with Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) regulations so institutions can avoid legal penalties.

· Effective CDD practices demonstrate the institution’s commitment to security and transparency, which builds customers’ and stakeholders’ trust.

Be Proactive Against Fraud with Brankas

For companies dealing with finance, it’s important to understand CDD’s meaning and role in mitigating fraud. By identifying, verifying, and monitoring customers through Customer Due Diligence and financial data API, organizations can significantly reduce the risks of fraudulent activities, and in doing so, strengthen people’s trust in the finance industry.

and How Does it Work?")